Financial statements built on maintained regulatory content

Prepare financial statements using pre-built, maintained frameworks, authored disclosure content and jurisdiction-specific logic. The result is faster preparation and confidence that local and global requirements are being met without complex configuration.

What firms achieve with Caseware

Confidence in local compliance

Prepare financial statements using ready-to-use frameworks aligned to IFRS and local GAAPs, maintained by Caseware.

Faster preparation with less rework

Reduce manual drafting, disclosure selection and template maintenance through automated logic and structured content for consistent financial statements.

Global reach without enterprise complexity

Support multi-national reporting with consistent workflows while respecting local standards, language and regulatory nuance.

Fast to deploy, easy to maintain

Deploy faster, train teams more easily and avoid the ongoing cost of maintaining highly customised reporting environments.

A practical approach to financial reporting at scale

Accurate content, clear structure and predictable outcomes across jurisdictions.

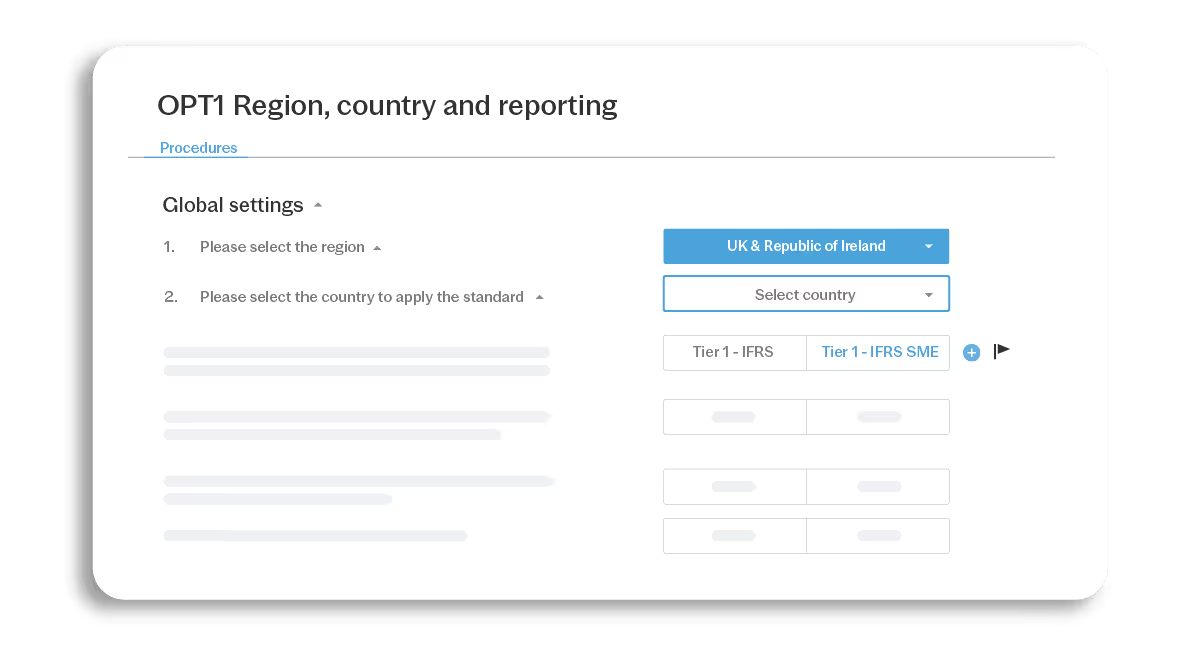

Use pre-built frameworks aligned to IFRS and local standards. Caseware invests directly in maintaining content and regulatory updates so firms and finance teams are not responsible for keeping templates current.

- IFRS and local GAAP coverage

- No custom template builds

- Ongoing regulatory updates

- Reduced compliance risk

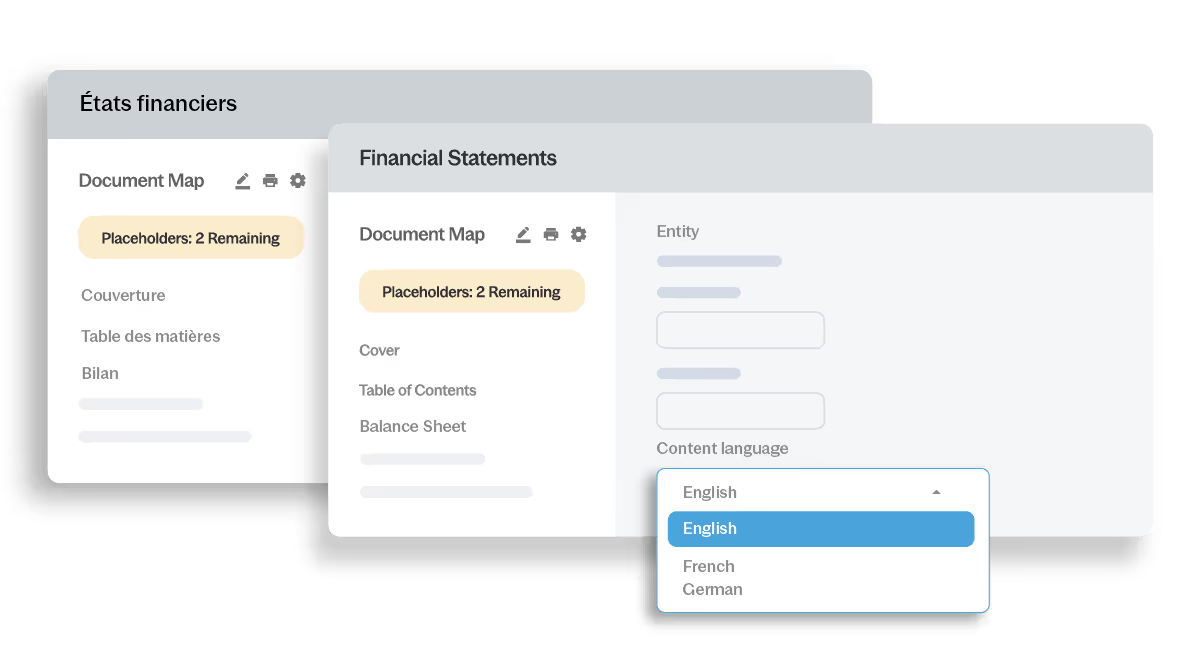

Prepare financial statements using professionally authored disclosure content in local languages. This ensures disclosures reflect regulatory intent, not automated translations.

- Authored local-language disclosures

- Jurisdiction-specific wording

- Consistent interpretation

- Reduced translation risk

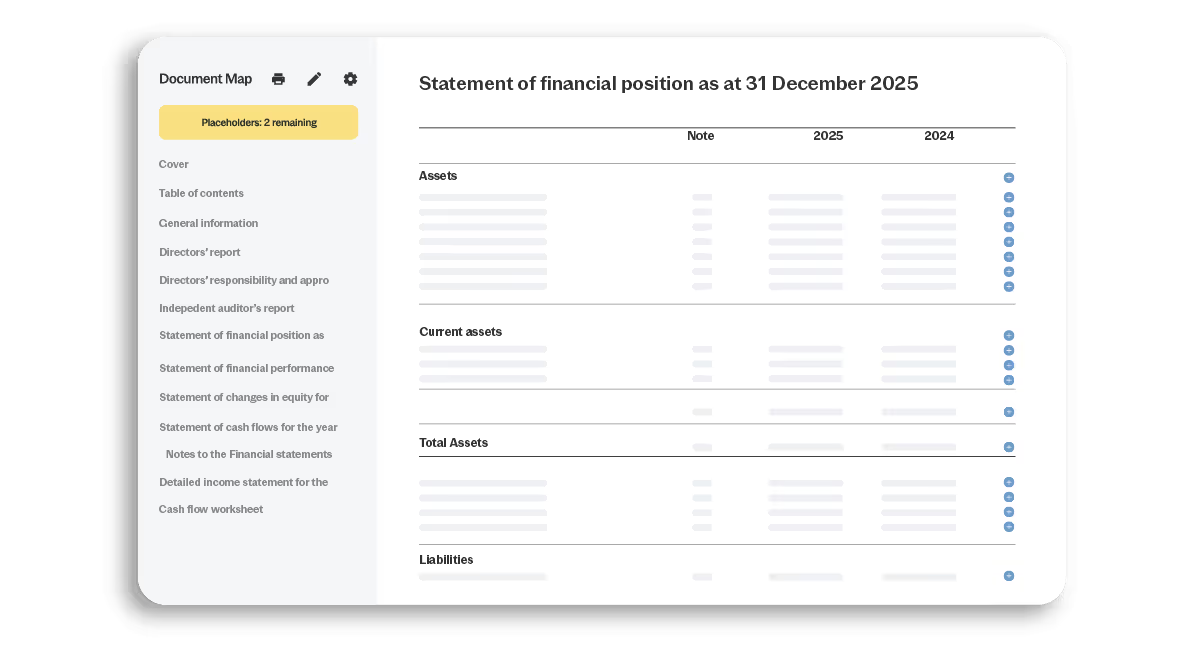

Generate financial statements and notes directly from imported trial balance data. Disclosure logic adjusts automatically based on entity size, scope and jurisdiction.

- Trial balance–driven drafting

- Dynamic disclosure logic

- Fewer missing disclosures

- Reduced manual effort

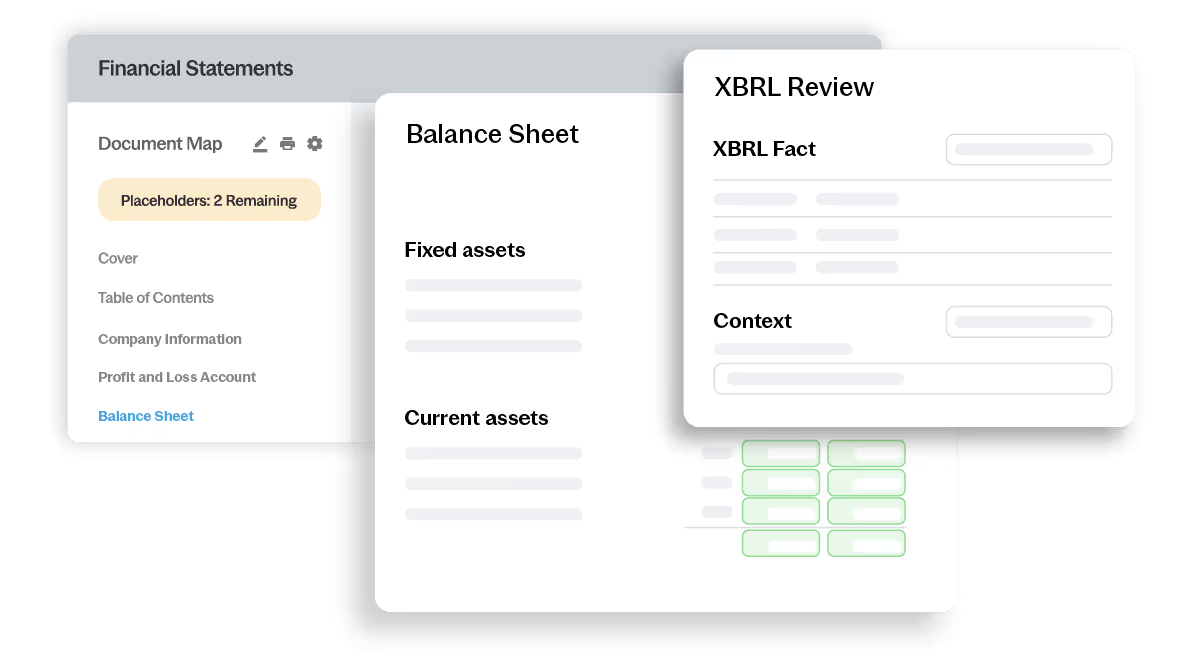

Financial statements are generated with jurisdiction-specific XBRL tagging applied as part of the reporting process. Review, refine and manage tags within the same file to support accurate, submission-ready outputs.

- Built-in XBRL and iXBRL tagging for relevant regions

- Jurisdiction-specific taxonomies

- Controlled tag review and overrides

- Filing-ready outputs

Related products

Frequently Asked Questions

Caseware invests directly in maintaining frameworks and disclosure content, delivering regular updates so users are not responsible for tracking and implementing regulatory changes.

Caseware prioritises ready-to-use content, faster deployment and lower complexity. This reduces implementation time, training effort and long-term cost while still supporting global scale.

Most teams can begin preparing financial statements quickly using pre-built frameworks and guided onboarding rather than lengthy configuration projects.

Automation links trial balance data, disclosure logic and reporting structure in one workflow. Built-in validation and review controls help surface inconsistencies earlier and reduce last-minute corrections.

Caseware supports export to Word, PDF and XBRL formats with jurisdiction-specific tagging applied. Outputs are structured to meet local filing and regulatory submission requirements.